Executive summary

Iran-related sanctions have entered a distinctly harder phase for corporates and banks operating in Türkiye and its surrounding trade corridors, driven by a convergence of

- A renewed U.S. “maximum pressure” architecture that explicitly directs Treasury to intensify designations and to scrutinize (and potentially tighten) licensing and guidance;

- The European Union’s re-imposition of wide nuclear‑proliferation‑linked restrictive measures following the September 2025 “snapback” sequence; and

- Enforcement and financial‑intelligence outputs that increasingly describe sanctions evasion as an industrial system—shadow fleets, exchange-house “shadow banking,” and procurement networks leveraging intermediaries in regional hubs.

For compliance leaders, the near-term practical consequence is that “Iran exposure” is no longer best assessed as a binary Iran/no‑Iran question; it is a network-risk question in which

- Maritime patterns (ship‑to‑ship transfers, AIS manipulation, opaque ownership, shifting flags),

- Payment pathways (exchange houses and front companies outside Iran, layered invoices, third‑party payments), and

- Procurement signatures (sensitive machinery, dual-use precursors, industrial software) are treated as enforceable proxies for Iranian nexus—often before a counterparty is publicly designated.

Recent U.S. actions explicitly target networks “based in Iran, Türkiye, and the UAE,” and list Türkiye-based entities as financial intermediaries in procurement chains, a fact pattern that should be treated as a compliance design input rather than an episodic headline.

Current sanctions landscape

The U.S. framework remains the most operationally consequential for globally connected firms because it combines a comprehensive embargo architecture (restricting U.S. persons’ dealings) with a mature, frequently used secondary-sanctions toolkit that exposes non-U.S. persons to designation or other measures for defined Iran-related conduct. The Office of Foreign Assets Control’s Iran program overview lists multiple statutory and executive authorities used to block persons and to target sectors of Iran’s economy (including via E.O. 13902) and repeatedly emphasizes that recent actions can be “subject to secondary sanctions,” a designation label that materially raises de-risking pressure in correspondent banking and trade finance.

Sectorally, current U.S. enforcement attention concentrates on revenue generation (petroleum and petrochemicals), logistics enablement (shipping, port services, and maritime insurance interfaces), and military/proliferation supply chains (precursor chemicals, sensitive machinery, and UAV-related networks), with transaction-based targeting that frequently follows behavioral indicators rather than stable corporate footprints. Treasury’s February 25, 2026 action describes sanctions on “over 30” persons/vessels enabling illicit petroleum sales and missile/advanced conventional weapons production, citing E.O. 13902, E.O. 13382, and E.O. 13949, and explicitly frames the action as part of a “maximum pressure” campaign.

The European Union has materially tightened its Iran posture since late 2025. On September 29, 2025, the Council stated it “reimpose[d]” nuclear‑proliferation‑related measures that had been suspended since 2015, explicitly describing the move as following the “reintroduction of the UN sanctions” after an E3 snapback invocation; the reintroduced measures include (among others) bans related to crude oil, gas, petrochemicals and related services; restrictions on key energy equipment; prohibitions on gold/precious metals/diamonds; and major financial-sector measures such as re-freezing assets of the Central Bank of Iran and major Iranian commercial banks.

In parallel, the EU’s Iran-related restrictive measures now span at least three large buckets relevant to regional firms:

- Nuclear proliferation measures (reimposed as above);

- Human-rights‑linked sanctions renewed and expanded since 2022 and extended to April 2026; and

- A dedicated framework (July 2023, expanded May 2024) targeting Iran’s drone/missile support to Russia and to armed groups in the Middle East/Red Sea region, with sanctions capable of listing suppliers and component providers.

In February 2026, the Council also decided to designate the IRGC as a terrorist organization under the EU counter-terrorism regime, increasing the legal and reputational sensitivity of any direct or indirect dealings involving IRGC-controlled value chains.

At the UN level, the applicable “sanctions state” is operationally complicated by an open, high-stakes legal and procedural dispute about snapback and the status of Resolution 2231’s timeline. Some Security Council members and UN-focused diplomatic statements characterize snapback as having legally reimposed earlier Iran resolutions and thus revived the 1737 committee workstream; Denmark, for example, states that “all sanctions against Iran were reimposed” following the Security Council vote and calls on Iran and all UN member states to comply with six reinstated resolutions. Other permanent members publicly reject that characterization; Russia asserts that Resolution 2231 expired on October 18, 2025, and that attempted snapback was “legally null and void,” treating the reactivation claim as unlawful. Iran’s foreign ministry likewise frames snapback as illegal and emphasizes that (in its view) Resolution 2231 terminated on the resolution’s own timeline. For compliance, this fragmentation matters less because U.S. and EU sanctions apply regardless of UN debate; however, the dispute directly affects how some jurisdictions may define “UN‑sanctions compliance” in procurement controls, port state control practices, and asset‑freeze screening.

Türkiye’s domestic sanctions posture is best understood as

- Implementation of UN Security Council measures through domestic administrative mechanisms, rather than

- A broad, autonomous Iran embargo comparable to U.S. or post‑snapback EU nuclear measures (while acknowledging that market participants in Türkiye may still adopt U.S./EU‑aligned controls to preserve correspondent and supply chain access).

An official Turkish “National Terrorist Asset Freezing Mechanism” document describes a Law No. 6415-based administrative mechanism to execute UNSC resolutions, with implementation roles described for MASAK and publication in the Official Gazette. In the current geopolitical environment—characterized by sustained regional conflict dynamics and Turkey’s expressed preference for de-escalation and mediation—this means local legal compliance baselines may remain anchored to UN lists, while commercial viability often requires “over-compliance” with U.S./EU expectations.

Comparative table: core Iran sanction regimes affecting Türkiye-linked business

| Dimension | US | EU | UN | Turkey |

| Administering authority & instruments | OFAC program architecture built on statutes + EOs; maximum pressure directives explicitly task Treasury with continual sanctions enforcement and potential license review. | Council reimposed nuclear proliferation measures in Sept 2025; maintains separate human-rights and drones/missiles frameworks; IRGC listed as terrorist org Feb 2026. | Legal status contested: some states assert snapback reimposed prior resolutions and revived committee reporting; others assert 2231 expired and snapback invalid. | Domestic mechanisms described for executing UNSC resolutions (asset freezes via administrative process; MASAK role; Official Gazette publication). |

| Primary scope for corporates | Comprehensive restrictions for U.S. persons plus sanctions exposure for non-U.S. persons via SDN and additional authorities targeting sectors, shipping, and procurement networks. | Post‑snapback nuclear measures cover trade/finance/transport; human rights measures include bans on internal repression equipment and telecom monitoring services; drones/missiles framework targets supply chains. | Where considered operative, would principally bind member states to implement revived lists and controls; practical impact varies by state due to dispute. | Primarily UN‑implementation lens; local regulatory risk is amplified by banks’ need to preserve foreign correspondent relations. |

| Secondary sanctions / extraterritorial bite | High; OFAC actions explicitly label certain sanctions as “subject to secondary sanctions,” and enforcement routinely targets third‑country intermediaries. | More territorial than U.S., but broad trade/finance bans and anti-circumvention principles create substantial third‑country compliance pull where EU counterparties, insurers, or banks are involved. | Extraterritoriality is via UN binding obligations on states, not direct enforcement against private actors; the dispute reduces uniformity. | No generalized secondary-sanctions equivalent; practical “pull” is indirect, via market access and counterparties subject to U.S./EU rules. |

| Sectors most relevant to Türkiye-region exposure | Petroleum/petrochem exports, shadow fleet logistics, exchange-house shadow banking, dual‑use procurement (chemicals/machinery/UAV components), and digital-asset pathways. | Energy trade bans and energy equipment controls; finance-sector freezes; drone/missile supply chain nodes; human rights-related internal repression goods/services. | If treated as revived: proliferation-related restrictions and listed entities; effects depend on local transposition/enforcement. | UN‑anchored targeted financial sanctions and controls; corporate exposure concentrated in banking, customs, logistics, and exports/transit monitoring. |

| Compliance posture signaled by recent actions | Frequent designations touching Türkiye-linked intermediaries; maritime guidance updated with explicit red flags and expectations for shipping/insurance/ports; enforcement releases illustrate diversionary sales, distributor schemes, and VPN-based evasion. | Post‑snapback reimposition plus expanded human rights and drones/missiles sanctions; IRGC terrorist listing increases scrutiny for any value chain overlap. | Split narratives and procedural friction at the Council level; compliance teams must treat UN measures as politically and operationally unstable. | Official messaging prioritizes de-escalation and mediation; domestic sanctions architecture described for UNSC implementation; commercial counterparties may still demand U.S./EU-grade controls. |

Drivers shaping trajectories

U.S. domestic politics is currently a primary driver because Iran sanctions policy has been re-anchored in a formal maximum-pressure memorandum that sets concrete operational tasks rather than general strategic intent. National Security Presidential Memorandum‑2 (February 4, 2025) directs Treasury to “immediately impose sanctions or appropriate enforcement remedies” where evidence exists, to run a “robust and continual” sanctions enforcement campaign denying revenue, to review for modification/rescission any general license or guidance providing relief, and to issue updated guidance specifically to shipping, insurance, and port operators—an instruction set that strongly predicts continuing designation volume and an elevated risk of policy tightening through guidance and licensing constraints.

JCPOA resurrection prospects, as a realistic driver of broad sanctions relief, appear structurally weak in the near term because

- The EU has already restored a sweeping pre‑2016 nuclear restrictive measures posture; and

- The “snapback” episode has produced an openly dual-track international legal narrative that reduces diplomatic bargaining space and increases the compliance cost of any partial normalization.

IISS analysis in late 2025 characterized the snapback step as a return to earlier mechanisms and constraints, while Chatham House commentary around the same period emphasized that looming snapback dynamics narrowed timelines for inspections diplomacy and raised the costs of delay.

Regional conflict dynamics are an accelerant because they directly connect to the legal justification narratives used in sanctions instruments and to the political feasibility of sustaining maximal enforcement. Türkiye’s foreign ministry statements in mid‑2025 and early‑2026 frame the security environment as involving attacks on Iran and Iranian targeting of third countries, urging cessation and emphasizing mediation; this aligns with a local policy preference for de-escalation, but it also underscores persistent security volatility that historically correlates with sanctions expansion and heightened trade controls. Brookings’ March 2026 analysis likewise frames the post-strike environment as one in which sanctions tools (including Global Magnitsky and related sanctions) are treated as “civilian levers of statecraft” alongside broader geopolitical moves, reinforcing an expectation that sanctions remain an active instrument rather than a frozen policy.

Iran’s behavior—especially nuclear transparency and enrichment posture—continues to be used as the formal trigger narrative for restrictive measures, and the “snapback legitimacy” dispute itself shows how quickly sanctions can shift based on compliance assessments by major powers. Denmark’s Security Council statement explicitly ties its snapback position to concerns about IAEA access and “highly enriched uranium stockpiles,” while the U.S. maximum pressure memorandum asserts breaches tied to undeclared sites/material and obstructed access, both of which suggest that “IAEA cooperation milestones” (or the absence of them) will be treated as sanction triggers in U.S./EU policy.

Russia/China ties affect Iran sanctions through two channels relevant to regional business: the procurement channel (dual-use goods and UAV proliferation) and the political channel (UN Security Council contestation and alternative financial rails). The EU’s sanctions page explicitly explains a dedicated framework targeting Iran’s military support for Russia’s war against Ukraine and for armed groups in the Middle East/Red Sea region, including the ability to target missile/drone components supply chains. Treasury’s February 25, 2026 action similarly frames designations against networks enabling Iran to secure sensitive machinery and to proliferate UAVs to third countries, which, for compliance design, is a clear warning that dual‑use and industrial procurement risk will remain an enforcement pillar.

Turkey’s policy posture is a driver not because it determines U.S./EU sanctions content, but because it shapes how risk concentrates operationally in Türkiye-linked trade, banking, and logistics. The Turkish MFA’s repeated emphasis on preventing escalation and offering mediation implies continued cross-border flows and sustained role as a corridor economy, while U.S. designation practice demonstrates that intermediaries in Türkiye are within the enforcement aperture for oil, shipping, and procurement networks (including through “financial intermediary” activity).

Scenarios and timelines

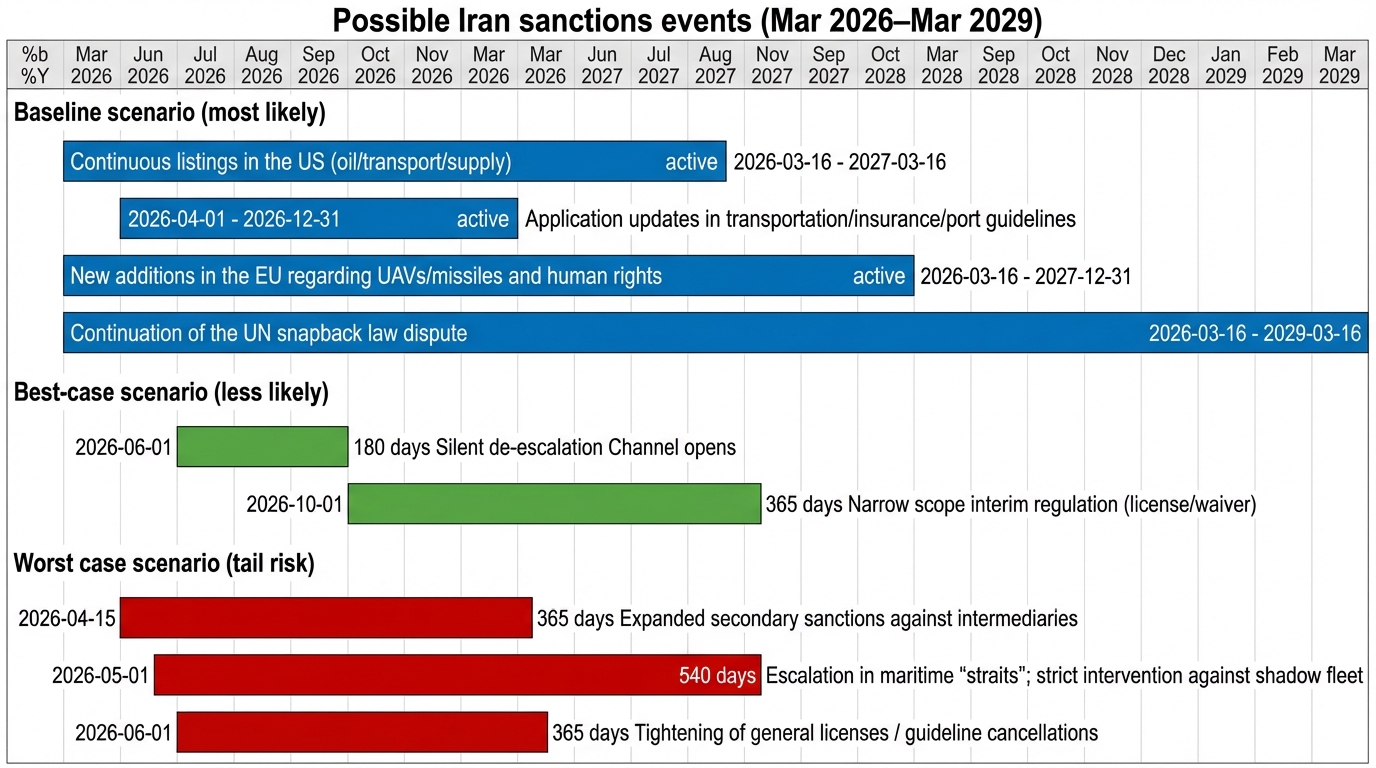

The most useful forecasting frame for compliance is not “will sanctions end,” but “how quickly do sanctions expand, and where will enforcement concentrate,” given that both U.S. and EU systems already support high-intensity restrictions. The following scenarios are structured around triggers that compliance functions can monitor and convert into decision thresholds.

In a best-case scenario, de-escalation channels re-open sufficiently to permit narrow, compliance-heavy arrangements that do not require wholesale rollback of the post‑2025 sanction posture. The most plausible best-case trigger set is: verifiable IAEA re-engagement and transparency steps viewed as meaningful by the U.S. and E3; a regional de-escalation path reducing proxy-linked attacks; plus a political premise inside the U.S. administration that sanctions relief is a lever worth trading for compliance. Even in this best case, NSPM‑2’s instruction to review and potentially rescind general licenses indicates that “license expansion” is not automatic; rather, relief would likely appear as tightly scoped, revocable licenses and waivers over humanitarian, safety, communications, and possibly limited energy stabilization logic, paired with intensified monitoring and snapback-ready clauses.

In the baseline scenario, sanctions intensity remains high and continues to rise incrementally through repeated designations and advisories, with limited licensing used mainly to manage safety, environmental, and wind-down externalities (especially in maritime contexts) rather than to reopen general commerce. This scenario is strongly supported by

- Treasury’s February 25, 2026 description of sanctions as a continuing “campaign of maximum pressure,”

- The EU’s reimposed nuclear trade/finance bans and the additional IRGC terrorist listing, and

- Sustained financial-intelligence emphasis on shadow banking and correspondent-account risk.

In this baseline, compliance pressure in Türkiye and the region increases primarily through counterparties’ de-risking behaviors (insurance refusals, documentary escalation, correspondent bank cutoffs) and through direct designation risk for regional intermediaries.

In the worst-case scenario, escalation triggers lead to “sanctions hardening” across both scope and enforcement tools: expanded use of secondary sanctions against non-U.S. firms (including those characterized as financial intermediaries), more aggressive targeting of shipping services (port operators, insurers, ship managers), and increased compliance demands for “know-your-vessel” and “know-your-customer’s-customer” (KYCC) practices. NSPM‑2 points directly to this pathway by instructing Treasury to evaluate beneficial ownership thresholds and by suggesting evaluation of KYCC standards for Iran-related transactions, while OFAC’s maritime advisory already frames evasive shipping as a systemic risk and calls for enhanced due diligence and controls. The worst-case timeline also anticipates deeper fragmentation of the UN position, increasing the chance that firms face conflicting “UN compliance” expectations alongside strict U.S./EU requirements, a complexity that typically increases compliance failure rates rather than reducing them.

Scenario matrix for decision-making

| Scenario | Timeline window | Triggers | What changes in practice for Türkiye-region firms |

| Best case | 6–18 months | IAEA cooperation milestones accepted by U.S./E3; credible de-escalation; political will to trade limited relief for verifiable steps. | Some narrowly scoped licenses/waivers may reappear, but with revocability and heightened reporting; compliance cost per transaction remains high. |

| Baseline | 12–36 months | Continued maximum pressure posture; persistent Iran oil/shipping and procurement networks; EU maintains post‑snapback stance and expands listings as needed. | Continual screening escalation; higher documentary burden; more frequent “false positive” escalations; increased de-risking by insurers and correspondent banks. |

| Worst case | 0–12 months onset, then persistent | Major escalation events; expanded targeting of intermediaries in transit hubs; aggressive secondary sanctions and KYCC expectations; intensified maritime enforcement campaign. | Higher probability of designation exposure for intermediaries; abrupt termination of relationships; trade freezes; increased seizures/impounds risk; extensive reputational contamination for indirect nexus. |

Compliance implications and risk mitigation for Türkiye-region firms

Compliance programs should treat current Iran sanctions risk as a “multi-regime, multi-vector” control environment where the strictest applicable rule-set is often set not by local law but by the most restrictive counterparty (correspondent bank, insurer, EU customer, U.S.-nexus vendor). The White House memorandum’s explicit instruction to review and potentially rescind general licenses, combined with OFAC’s use of narrow safety and environmental general licenses for maritime-specific issues (as reflected in Federal Register-published web general licenses), means that reliance on historical “business-as-usual” interpretations is a liability: controls must be continuously refreshed against the most recent guidance and licensing posture.

For trade and industrial firms, the key shift is that “Türkiye as an intermediary jurisdiction” is now a first-order risk factor in U.S. procurement enforcement narratives, not a background consideration. Treasury’s February 25, 2026 action describes Türkiye-based companies serving as “financial intermediaries” for procurements involving “sensitive machinery” relevant to advanced conventional weapons platforms, and the action is framed as part of broader nonproliferation designations. This matters because many general industrial goods—machine tools, industrial pumps, control systems, specialized chemicals—sit near dual-use thresholds; enforcement risk arises when a transaction is structured to conceal end use or end user (e.g., layering through distributor hubs, re-export pathways, or third-country invoicing). Firms should implement a two-layer control: classification control (export controls / dual-use lists and internal restricted goods lists) plus transaction-context control (unusual payment routes, offshore intermediaries, lack of plausible end-use narrative, or a customer unwilling to provide end-user declarations).

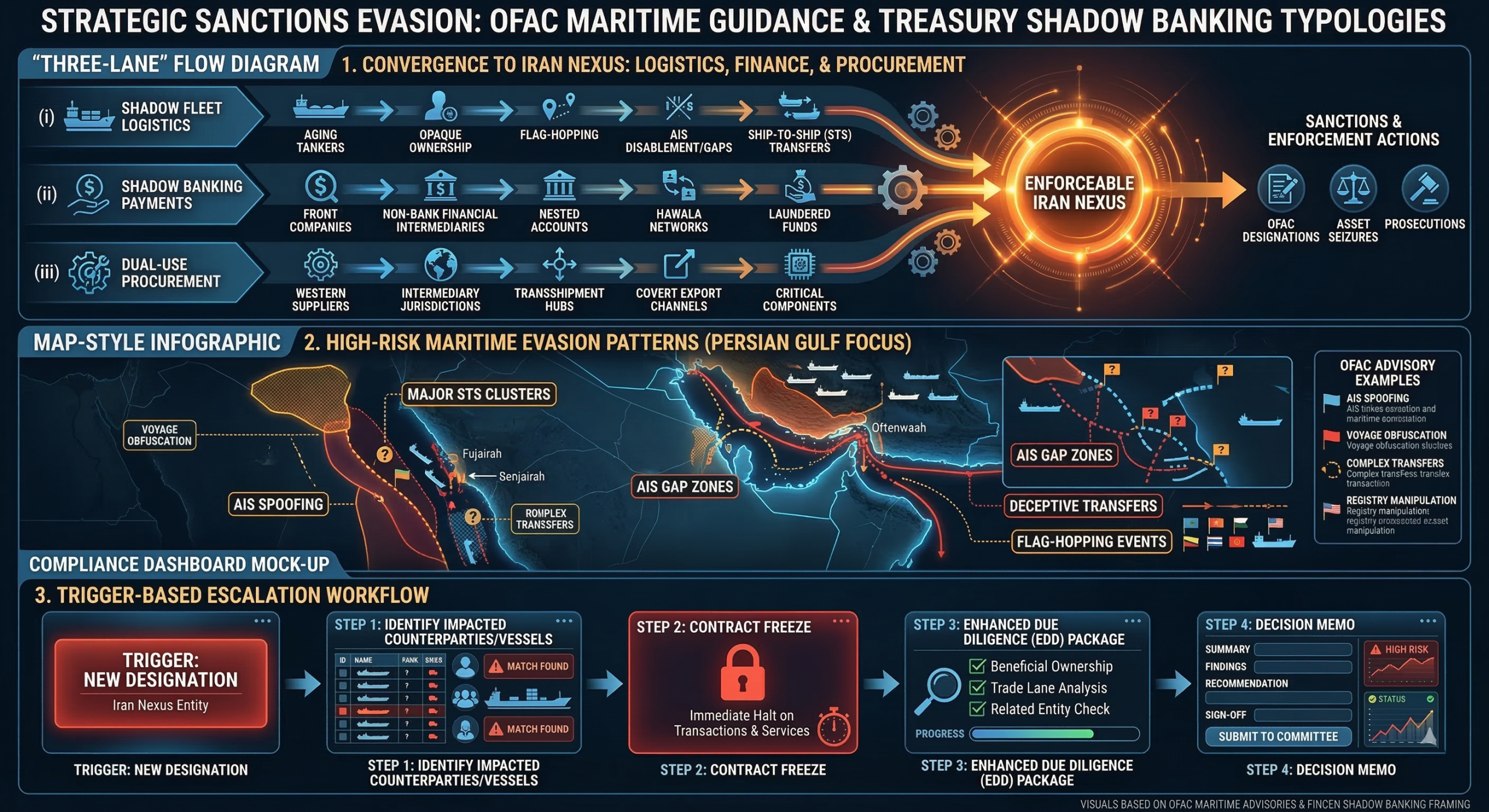

For banks and payment intermediaries, the “shadow banking” evidence base is now strongly articulated in U.S. financial intelligence outputs, and it is directly relevant to correspondent banking risk for Türkiye-linked institutions even absent local sanctions prohibitions. FinCEN’s October 2025 release states it identified approximately $9 billion of potential Iranian shadow banking activity in 2024 flowing through U.S. correspondent accounts and describes the typology: Iran-based exchange houses and foreign front companies (prominently in the UAE, Hong Kong, and Singapore) moving money to evade sanctions, launder proceeds, and fund weapons/proxy activity. Treasury’s June 2025 press release further explains that such systems operate as a parallel banking system using front companies and fictitious invoices/transaction details, a description that should be operationalized into transaction monitoring rules (e.g., repeated third-party payments with thin commercial rationale; front-company clusters transacting heavily with each other; sudden spikes in activity linked to commodity trades where documentary quality degrades).

For shipping, ports, logistics providers, and their banks and insurers, the decisive compliance imperative is that OFAC’s April 2025 maritime advisory is no longer “nice-to-have guidance”; it describes enforceable risk expectations, including specific deceptive practices and due diligence actions. OFAC highlights that Iranian tankers use multiple ship-to-ship (STS) transfers—often three to five—to obscure origin and sanctionable involvement, particularly when combined with night operations, unsafe waters, proximity to sanctioned jurisdictions/terminals/refineries, or missing/manipulated AIS data; it also explicitly flags document falsification (bills of lading, certificates of origin, invoices, port-of-call lists) and complex ownership structures using shell companies/SPVs in low-transparency jurisdictions. Banks financing shipping-linked trades should therefore treat vessel behavior analytics (AIS consistency, STS frequency, flag changes) and ownership transparency as credit risk variables, not only sanctions screening inputs.

Compliance leaders should also internalize that enforcement actions increasingly punish organizational and cultural failures (lack of monitoring, obfuscation, willful circumvention) at least as much as they punish technical screening errors. OFAC’s enforcement releases provide concrete pattern evidence: Harman’s case involved product diversion from a UAE distributor to Iran with internal obfuscation language (“northern region,” “North Dubai,” “up north”), reflecting the risk of euphemisms and end-market concealment in distributor management; Unicat’s case involved use of overseas affiliates and shipments routed from China to supply Iranian end users; Exodus’ case illustrates the digital compliance analog—staff recommending VPNs to help users in Iran bypass sanctions controls; and the Fracht case shows how logistics urgency and third-party brokers can lead to dealings with blocked airlines and Iran-linked aircraft. These cases support an explicit mitigation step: embed sanctions controls into commercial compensation and distributor governance (contractual restrictions, audit rights, termination triggers), and train staff on “soft evasion signals” such as euphemistic geography, reluctance to disclose end users, and pressure for urgency that bypasses controls.

For firms operating in Türkiye specifically, a realistic compliance position is that local law implementation mechanisms (asset freezing and UNSC execution) should be treated as the floor, while U.S./EU expectations are the ceiling if the firm touches U.S. dollar clearing, EU customers, Western insurers, or multinational supply chains. Türkiye’s official documentation describes an administrative mechanism for executing UNSC resolutions and asset freezing with roles for MASAK and Official Gazette publication; in practice, however, the more immediate commercial risk often comes from foreign counterparty de-risking decisions based on perceived Iran nexus, even where Turkish law would not prohibit a transaction. The correct mitigation response is to document the firm’s rule hierarchy, escalation process, and decision rationales so that de-risking or transaction rejection is defensible to business heads and regulators alike.

Enforcement risk indicators, red flags, and monitoring workflow

Maritime and commodities red flags should be treated as “high-confidence” indicators because they are articulated in OFAC’s own guidance: repeated STS transfers (especially multiple sequential transfers), AIS disablement or manipulation, inconsistent or rapidly changing vessel identity data (MMSI/IMO mismatches), and complex/opaque vessel ownership and management structures using shell entities in low-transparency jurisdictions. Document integrity is a second cluster: suspicious certificates of origin, invoices with nonstandard commodity descriptions, bills of lading that do not match vessel routing, and port-of-call lists inconsistent with AIS tracks. Where a firm’s exposure includes petroleum/petrochemical trades, OFAC explicitly recommends cargo-origin verification measures, including enhanced documentation requests and analytical verification steps, which can be operationalized as a mandatory enhanced due diligence (EDD) gate for high-risk cargoes.

Financial and correspondent-banking red flags in the current cycle are best derived from FinCEN’s shadow banking characterization: repeated use of exchange houses or exchange-house-linked corporates; front companies in known hubs transacting in circular patterns; layered third‑party payments with weak or generic invoice narratives; and sudden, high-volume flows connected to commodity sales where the commercial counterparties appear unrelated or newly formed. FinCEN’s framing that Iranian shadow banking transacts “billions of dollars” with each other and with potentially unwitting companies implies that “wittingness” is not a safe harbor; banks should implement typology-driven monitoring scenarios and risk-rate customers whose business models are structurally compatible with exchange-house settlement.

Trade and procurement red flags in Türkiye-region operations should incorporate the enforcement fact pattern that U.S. authorities now openly describe: intermediaries serving as financial conduits for sensitive machinery or precursor chemical procurement for missile and advanced conventional weapons programs. Practically, this translates into EDD triggers such as: customer requests for “generic machinery” inconsistent with the customer’s sector; unwillingness to provide end-user or installation site details; split shipments; use of unrelated trading companies as invoice issuers or payors; and payments originated by third parties (or by small firms with no plausible source of funds) that appear to be “financial intermediaries” rather than commercial buyers.

Digital-asset red flags have moved from theoretical to enforceable; OFAC’s Exodus settlement demonstrates that providing services to persons in Iran—including support enabling access to third-party exchanges—and recommending VPN usage to evade sanctions controls can form the basis of significant penalties and “egregious” findings. Compliance programs in fintech-adjacent corporates (including marketplaces, SaaS providers, and logistics platforms) should therefore treat geolocation management, sanctions-screening of users and counterparties, and “sanctions circumvention assistance” training as core controls, not “financial sector only” measures.

Monitoring should be formalized as a source-governed workflow rather than ad hoc browsing. At minimum, the monitoring stack should include: OFAC’s Iran program page and “Recent Actions” feed (for new designations and general licenses), OFAC enforcement releases (for typology learning), and FinCEN releases and analyses (for shadow banking and correspondent-risk typologies). On the EU side, the Council’s sanctions pages and press releases provide primary, citable updates on the scope of restrictive measures (including the post‑snapback nuclear measures and IRGC terrorist listing). On the Türkiye side, official MFA statements are essential for geopolitical baseline assumptions that affect sanctions risk (e.g., escalation, mediation posture), while Turkish UNSC-implementation materials describe the domestic architecture relevant for asset-freeze compliance and related administrative risk.

A practical due-diligence control set for corporates and banks operating in/with Türkiye should be structured as a repeatable “Iran nexus triage” that prevents both over blocking and under blocking:

- Sanctions list screening of all counterparties, beneficial owners, directors, and key third parties (agents, brokers, freight forwarders, ship managers), using consistent name standards;

- Sessel-level screening using IMO numbers and behavioral analytics (AIS continuity checks, STS patterns, flag history) for any sea-borne commodity exposure;

- End-use/end-user certification plus plausibility testing for any machinery, chemicals, electronics, or industrial software near dual-use thresholds;

- Payment pathway mapping to detect exchange-house settlement, third-party payments, and circular flows; and

- Escalation protocols that explicitly document why a transaction is cleared, rejected, or licensable, acknowledging that U.S. policy now directs intensification of enforcement and potential tightening of general licenses.