Executive summary

The current US–Israel–Iran crisis has escalated into overt interstate warfare with immediate, measurable effects on global energy prices and shipping risk premia. US and Israeli officials describe a multi-domain campaign intended to destroy Iranian missile and naval capabilities and remove any nuclear-weapons pathway; Iran characterizes the strikes as unlawful aggression and asserts a right of self‑defence under the UN Charter. The operational center of gravity for global markets is not simply damage to facilities inside Iran, but the real or perceived ability of Iran (and aligned forces) to disrupt exports and transit through the Strait of Hormuz at scale, and to raise war-risk costs to the point that commercial shipping becomes non-viable.

Energy markets are reacting through three channels that reinforce one another: (i) physical risk to supply (production curtailments and LNG outages), (ii) transit and insurance denials that convert “available supply” into “undeliverable supply,” and (iii) a volatility shock that pulls forward risk pricing into prompt contracts. In the first week of fighting, Brent and WTI spot prices jumped sharply, European gas benchmarks surged, and LNG freight rates spiked—consistent with a classic chokepoint/insurance mechanism rather than a slow-moving supply–demand rebalancing.

From a defense-legal perspective, the most consequential “next decision points” are (a) whether Hormuz is effectively closed by violence or commercial withdrawal; (b) whether strikes expand to major Gulf export hubs and processing nodes (especially Qatar’s Ras Laffan complex, which is central to global LNG); and (c) whether outside states operationalize collective self-defence in ways that normalize interdiction or quasi-blockade conditions. Price outcomes over the next 2–12 weeks are therefore best treated as scenario‑conditional distributions rather than point forecasts: in my assessment, the modal outcome remains a “high-volatility, partial-transit denial” regime that keeps crude oil and European gas materially above pre-war baselines, with fat‑tail upside if the transit/insurance channel hardens into a sustained blockade-like reality.

Current strategic picture and declared objectives

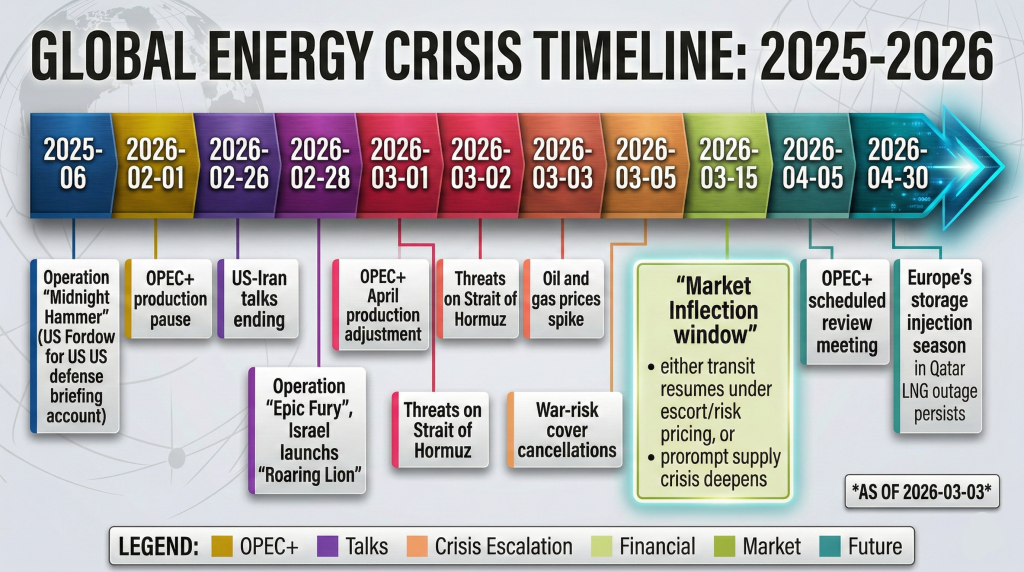

The publicly stated US posture is that combat operations began on 28 February 2026 under “Operation Epic Fury,” directed at Iran’s command-and-control nodes, air defenses, missile and drone launch sites, military airfields, and naval forces. U.S. Central Command describes the strikes as ordered by Donald Trump and framed as responsive to Iranian threats and attacks, emphasizing the initial target set and the start time of the operation. US defense messaging (including a Pentagon briefing account published on the official defense news portal) stresses “laser-focused” objectives—destroy offensive missiles, missile production, and elements of Iranian naval/security infrastructure—while asserting “no nukes” as an end state and explicitly rejecting “nation-building.” The The White House has amplified this framing in a “Peace Through Strength” narrative that ties the operation to ending an “Iranian regime” nuclear threat and protecting US personnel and allies.

Israeli operational communications describe a parallel campaign (“Operation Roaring Lion”) with real-time strike reporting. The Israel Defense Forces update feed emphasizes waves of strikes on missile launchers, aerial defense systems, command centers, and regime-linked infrastructure in and around Tehran, while also reporting defensive intercept activity and spillover engagements (including strikes against Hezbollah targets in Beirut). In diplomatic reporting, Israel’s UN envoy has publicly reiterated that preventing Iranian nuclear capability is a core objective and that joint operations will continue until that condition is achieved (with the usual caveat that battlefield claims and attribution—especially regarding civilian casualties—can be difficult to verify in wartime).

Iran’s official diplomatic line is anchored in jus ad bellum: the Ministry of Foreign Affairs describes the US and Israel strikes as a “gross violation” of sovereignty and territorial integrity, explicitly invoking Article 2(4) of the UN Charter and asserting a “legal and legitimate right” of self-defense under Article 51. Iran also claims the attacks occurred “in the midst of a diplomatic process,” positioning itself as having pursued talks while preparing for defense, and calls on the UN Security Council to act. In a parallel, highly market-relevant line of effort, senior IRGC-linked statements reported by Reuters assert that the Strait of Hormuz is closed and threaten to strike vessels attempting passage—an escalation designed to convert military pressure into global economic pressure.

International official reactions split along familiar fault lines but converge on escalation risk. António Guterres condemns the escalation and reiterates that the UN Charter prohibits the threat or use of force against territorial integrity or political independence, calling for cessation of hostilities and return to negotiations. China’s Foreign Ministry goes further, describing it as unacceptable to strike during negotiations and to “attack and kill a leader of a sovereign country,” calling for an immediate stop and return to dialogue, while supporting Iran’s defense of sovereignty and warning against “law of the jungle” dynamics. The EU and E3 statements, meanwhile, condemn Iranian regional strikes and stress protection of civilians and freedom of navigation, while warning that disruption of the Strait of Hormuz must be avoided and signaling additional sanctions tools.

How this conflict transmits into oil and gas prices

The geometry of energy risk in this conflict is dominated by chokepoints. Strait of Hormuz alone carried roughly 20.9 million barrels per day of crude/condensate/products in 2023 and about 10.4 Bcf/d of LNG flows, per the US government’s chokepoints analysis. This is why even “partial” interference can produce nonlinear price reactions: when supply and demand are short-run inelastic, the price must move a great deal to equilibrate the market in the face of a sudden deliverability shock.

Physical disruption in the first week has already extended beyond rhetoric. Reuters reports attacks on Gulf energy infrastructure and tankers, with operations halted across multiple producers and exporters, and insurance coverage suspended such that tankers avoid the area—turning a military contest into an immediate logistics constraint. A separate Reuters dispatch highlights that major Japanese shipping companies halted Hormuz operations, underscoring that “availability of crude” is not the same as “ability to lift and deliver it.” For gas, the core mechanical link is Qatar: it is a top global LNG exporter (about one-fifth of global LNG exports by Reuters’ accounting) and its Ras Laffan complex concentrates liquefaction capacity. Ras Laffan is now reported as impacted, with LNG production suspended, forcing the world’s LNG market to reprice scarcity in prompt cargoes and transport.

Sanctions amplify these mechanics by narrowing the “legal” and “insurable” supply set. The U.S. Department of the Treasury, through Office of Foreign Assets Control, announced broad designations targeting Iran’s “shadow fleet” and procurement networks for ballistic missiles and advanced conventional weapons, citing authorities under multiple executive orders and explicitly tying oil revenues to weapons programs and proxy financing. Even absent new kinetic damage, such steps raise transaction costs, reduce compliant shipping capacity (as counterparties de-risk), and can widen differentials between sanctioned and non-sanctioned barrels.

Insurance and reinsurance decisions are the most direct commercial chokepoint. In the past 72 hours, multiple protection-and-indemnity actors issued cancellation notices for war risks in Iran and the Persian/Arabian Gulf, defining covered waters expansively (including the Gulf of Oman west of a specified line) and setting near-term effective dates. Japan P&I Club and UK P&I Club provide formal notice structures that effectively tell shipowners: trade may continue only under bespoke write-backs or alternative insurance, at sharply higher premia, and with uncertain claims treatment. Gard issued a similarly structured notice, which—combined with contemporaneous reporting of insurers withdrawing cover—creates a market-wide brake on tanker and LNG movements. This is why LNG freight rates could jump more than 40% in a day: risk premia are being repriced not as marginal cost, but as existential voyage feasibility.

Market psychology does not operate independently of fundamentals here; it accelerates them. EIA’s crude oil market framework explicitly notes that geopolitical events can create uncertainty about future supply and demand, increasing volatility, and that large price changes can be necessary when supply and demand cannot adjust quickly. In this case, the “uncertainty premium” becomes self-fulfilling through precautionary buying, refined-product crack expansion, and front-end curve stress. Reuters reports sharp moves not only in crude but also in diesel and European gasoil futures, consistent with a deliverability shock into refined products and shipping constraints.

A concise exposure map is useful for quantifying why the market is reacting so fast:

| Route / node | Oil flow (2023) | LNG flow (2023) | Why it matters in this conflict | Notes on substitutes |

| Strait of Hormuz | ~20.9 mb/d | ~10.4 Bcf/d | Central transit artery for Gulf crude/products and Qatar LNG; threats/attacks here convert supply into “undeliverable supply.” | Pipeline bypass capacity from Saudi/UAE estimated ~2.6 mb/d in disruption scenarios—material but far below total exposure. |

| Suez Canal + SUMED | ~8.6 mb/d | ~4.0 Bcf/d | Secondary chokepoint for Gulf-to-Europe and broader trade patterns; disruption compounds freight and delivery times. | Diversion via Cape of Good Hope increases transit time and cost substantially. |

| Bab el-Mandeb | ~8.6 mb/d | ~4.0 Bcf/d | Red Sea access point; risk of compounded disruptions (especially if regional actors expand attacks). | Diversion around Africa is feasible but costly and slow; insurance premia rise. |

Price outlook with confidence levels and scenario ranges

Baseline conditions before the shock

Pre-war agency outlooks did not price in a sustained Hormuz shut-in. The International Energy Agency expected world supply growth to outpace demand in 2026, with inventories building, even after weather-related disruptions in early 2026. The U.S. Energy Information Administration February STEO forecast Brent averaging about $58/b in 2026 (and $53/b in 2027), explicitly acknowledging that a conflict affecting flows through the Strait of Hormuz “could obviously reduce Middle East oil production and exports.” The International Energy Forum comparative summary underscores that even among IEA/OPEC/EIA there was divergence on 2026 levels, but not a baseline assumption of a chokepoint closure.

That matters because it tells you what the market is now paying for: optionality and tail risk, not incremental tightening. Current prices around $80–$85 Brent are therefore best read as (i) a rapid “risk premium” repricing, and (ii) an early signal that prompt barrels and LNG cargoes are perceived as scarce under current logistics constraints.

Short- and medium-term forecasts

As of 3 March 2026, spot and futures indicators show a sharp front-end move: Brent and WTI spot surged; European gas benchmarks jumped; and major-venue futures prints show elevated levels (e.g., Dutch TTF calendar-month futures around the high‑50s €/MWh and Henry Hub front-month futures around $3.17/MMBtu at the time of the CME snapshot). Those values will remain dominated by military and insurance decisions for at least the next 2–6 weeks.

I therefore present scenario‑conditional ranges rather than a single point estimate. The confidence levels below reflect (a) the number of independent mechanical links (chokepoint, insurance, storage) pointing the same direction, and (b) the inherently political nature of the stopping condition.

| Horizon | Crude oil (Brent) | Natural gas (Europe TTF) | LNG (Asia JKM proxy) | Confidence (direction / range) | What chiefly drives the band |

| Next 2 weeks (to mid‑March) | $80–$120/b | €50–€90/MWh | High volatility; +20–60% vs pre-war prompt | High / low–medium | Whether Hormuz becomes commercially non-viable under attack/insurance withdrawal; whether Qatar output resumes quickly. |

| Next 2–3 months (to end‑May) | $70–$110/b | €45–€85/MWh | Tightness persists if Qatar outage extends | Medium / low | Re-establishment of insurable convoy/escort patterns; OPEC+ supply response; emergency stock releases. |

| Next 6–9 months (to end‑2026) | $60–$95/b | €35–€80/MWh | Dependent on Europe storage refill success | Low–medium / low | Whether the war ends with restored freedom of navigation or entrenched maritime denial; durability of sanctions and infrastructure damage. |

These ranges are anchored by three observable facts. First, agency baselines implied much lower 2026 averages absent a chokepoint crisis.

Second, Reuters reports that analysts are already modeling $120–$150 Brent in a prolonged conflict scenario—consistent with a multi‑month transit denial rather than a brief scare.

Third, Europe’s gas system is entering injection season from a weak storage position (Germany around 27% and the Netherlands around 10% at the start of March per Reuters’ reporting), which structurally increases the price sensitivity to LNG outages and rerouting.

Scenario analysis with triggers, timelines, and quantified ranges

| Scenario | Military / political trigger set | Timeline logic (what changes first) | Brent crude range | European gas (TTF) range | Strategic “stopping point” |

| Best case | Rapid de-escalation: negotiated pause; no sustained tanker attrition; insurers reinstate cover or states provide credible security that restores underwriting. | Shipping resumes within 7–14 days; Qatar liquefaction restarts; prompt risk premium collapses faster than medium-term curves. | $65–$80 | €35–€55 | A ceasefire/stand‑down plus publicly verifiable transit security (de-mining, escorts, and underwriting normalization). |

| Most likely | Protracted high-intensity phase but without full, sustained physical closure: intermittent attacks and war-risk denial create an uneven “stop–start” trade pattern; partial resumption under escort at high premia. | Tanker queues and “shadow capacity” emerge; refined-product shortages appear regionally; OPEC+ offers limited stabilization via incremental supply and rhetoric. | $80–$110 | €50–€85 | A tacit bargain that deters attacks on neutral shipping and critical export nodes, even if land strikes persist. |

| Worst case | Effective blockade/closure dynamics: sustained attacks on tankers and ports; formal or de facto mining; major Gulf LNG and oil export infrastructure remains offline; conflict expands with collective self-defence strikes “at source.” | Immediate commercial withdrawal hardens; inventories draw rapidly; governments intervene with stock releases and demand restraint, but logistics remain constrained. | $120–$160 (spikes possible above) | €80–€150 | Either (i) enforced maritime corridor under major-power naval control, or (ii) negotiated termination that restores an insurable operating environment. |

Substitutes and mitigation measures with feasibility, cost, and timescales

Mitigation capacity exists, but it is asymmetrical: oil has meaningful emergency stocks and some rerouting ability; LNG is less forgiving because liquefaction outages and shipping denials cannot be “inventoried” quickly on the consumer side, especially when storage is low.

The practical question is not “can supply be replaced,” but “how much deliverable energy can be brought to market within the time constant of panic and storage drawdown.”

| Mitigation lever | What it substitutes (and how) | Feasibility | Fastest plausible impact | Cost & constraints (practical, not theoretical) |

| Emergency oil stock release (IEA collective action) | Adds prompt barrels to offset sudden crude/product shortages; reduces panic and smooths refinery feedstock availability. | High (policy-dependent) | Days to a couple of days for decision, then releases begin. | Politically constrained; cannot “solve” a long closure—only buys time; effectiveness depends on refinery compatibility and shipping. |

| US Strategic Petroleum Reserve | National emergency drawdowns; historically used during wars and disruptions; current stock reported ~415 million barrels (capacity ~714 million). | Medium–high | Days–weeks | Quality mix (sour vs sweet), drawdown rates, and political willingness shape impact; not a substitute for LNG shortfalls. |

| Pipeline bypass around Hormuz (Saudi/UAE) | Shifts crude to Red Sea / Gulf of Oman export points; EIA estimates ~2.6 mb/d bypass capacity may be available in disruption scenarios. | Medium | Weeks (operational ramp) | Limited relative to ~20 mb/d exposure; still vulnerable to downstream chokepoints (Bab el‑Mandeb/Suez) and to strikes on terminals. |

| LNG cargo redirection / demand bidding | Redirects LNG from lower-priced basins to Europe/Asia; relies on flexible volumes and shipping availability. | Medium in theory, low under shipping denial | 1–6 weeks | If Qatar (≈20% of global LNG exports per Reuters) is offline, flexibility shrinks; freight, canal routing, and insurance constraints dominate. |

| Fuel switching and demand restraint | Substitutes gas for oil (or coal for gas) in power/industry; reduces demand under emergency regimes. | Medium (sector-specific) | Weeks to months | Often requires regulatory relaxation or operational capability; demand destruction is economically costly and politically sensitive, but effective when prices surge. |

| Accelerated renewables and efficiency | Reduces marginal gas burn and peak power demand; offsets import needs over time. | Medium (deployment lead times) | Months to years | Not a short-run crisis tool; however, it affects medium-term forward expectations and security policy incentives. |

The oil side of the ledger is therefore “bufferable but not painless,” while the gas/LNG side is “tight and timing-sensitive.” This is why Europe’s storage position (Germany ~27% vs ~64% typical for early March, and the Netherlands ~10% vs ~48% average in Reuters’ data) is a critical determinant of how far TTF can overshoot in a prolonged Qatar/Hormuz disruption.

Legal and defense constraints shaping energy infrastructure and trade

Maritime law: transit passage, blockade logic, and the grey zone

The law governing straits used for international navigation is designed to prevent exactly the kind of chokepoint coercion now being signaled. Under UNCLOS Part III, ships and aircraft enjoy a right of transit passage through such straits, and that transit passage “shall not be impeded.” In practice, a belligerent can still create de facto impediment through mines, drone boats, or credible threats—without issuing a formal blockade declaration—forcing coastal states and naval powers into a choice between (i) escalation to enforce navigation, (ii) acceptance of a “closed strait” reality, or (iii) negotiated deconfliction that trades military objectives for economic stabilization.

A formal blockade framework (as reflected in the San Remo Manual) illustrates why “closure by threat” is legally and operationally fraught. A blockade must be declared and notified, must be effective as a matter of fact, must not bar access to neutral ports/coasts, and must not have a sole purpose of starving civilians; merchant vessels believed to be breaching it may be captured, and—after warning—attacked if they clearly resist capture. This matters for energy markets because any drift toward blockade-like enforcement (even if never labeled a blockade) increases the probability of vessel search, diversion, capture, or attack—raising freight, demurrage, and insurance costs as a structural feature, not a temporary spike.

Mining risk is particularly destabilizing because it converts a navigational issue into a clearance-time issue. The San Remo Manual’s treatment of mines emphasizes notification and neutralization constraints and underscores that transit passage through international straits should not be impeded unless safe and convenient alternative routes are provided—an impossible standard where geography offers no true alternative. The market implication is straightforward: even a small number of mine-like events can produce prolonged commercial withdrawal because clearance and “insurability restoration” are slower than price moves.

Sanctions law and compliance risk as a supply constraint

Sanctions are not merely punitive; they are market-structuring. OFAC’s February 2026 action targeting Iran’s shadow fleet and procurement networks illustrates how petroleum flows, shipping registries, and financial intermediaries become part of the operational battlefield. When the US designates vessels and entities connected to Iranian petroleum sales, it increases the compliance risk borne by banks, insurers, charterers, and ports—even for transactions that might otherwise seem “commercially rational.” The EU’s statement signaling continued and possibly expanded sanctions, alongside calls for maritime security and freedom of navigation, indicates that the compliance environment is likely to tighten rather than loosen while the conflict persists.

For energy infrastructure investors and traders, the legal risk is not confined to the sanctioned counterparty. It extends to beneficial ownership opacity, documentation integrity, and the ability to obtain war-risk and P&I cover. The formal cancellation notices by major P&I-linked actors demonstrate that even where sanctions do not prohibit a voyage, insurance may still make it commercially impossible.

Targeting law: energy infrastructure as “dual-use” and proportionality pressure

From an operational law perspective, energy infrastructure sits at the intersection of military necessity and civilian protection. Under customary IHL, attacks must be directed at military objectives—objects which, by their nature, location, purpose or use make an effective contribution to military action and whose destruction offers a definite military advantage; even then, proportionality prohibits attacks expected to cause incidental civilian harm excessive in relation to the concrete and direct military advantage anticipated. In modern conflicts, refineries, ports, power grids, and communications nodes are frequently “dual-use,” meaning legal assessments become facts-intensive and contestable; the strategic consequence is that targeting decisions can rapidly become alliance-liability issues, not only battlefield choices, because they shape third-state reactions, sanctions legitimacy narratives, and the willingness of insurers and shippers to resume trade.

Iran’s MFA statement and multiple third-party official statements (EU/E3/China/UN) show that legality narratives are already a primary battlespace, not an afterthought. For energy markets, “legality contestation” matters because it drives whether states treat maritime escort, interception, or strikes “at source” as legitimate collective self-defence—or as escalatory acts that broaden the war.

Winners and losers across sectors and states

The near-term winners are those positioned to monetize price spikes without needing Hormuz transit: non-Gulf producers with export flexibility, certain diversified traders, and segments of the defense and security ecosystem tied to air/missile defense and maritime security demand. Refiners can be mixed winners/losers: higher crack spreads may benefit some, but feedstock volatility, shipping constraints, and demand destruction can overwhelm margins, particularly where product exports rely on disrupted routes.

The largest losers are import-dependent consumers facing prompt-price exposure, especially where storage is low and supply is inflexible. Europe is structurally vulnerable on gas because storage must be refilled into a global LNG market that is now short a major supplier (Qatar) and constrained by shipping risk. Asian LNG importers are exposed through contracted dependence on Qatar and through the fact that much Hormuz LNG historically flows to Asia; that concentration makes any prolonged disruption a price setter for JKM-linked markets.

Shipping and insurance are “winners by price, losers by risk.” Freight and war-risk premia can surge (as evidenced by LNG freight jumps and war-risk cancellation notices), but the sector’s profit opportunity is bounded by the possibility of voyage cessation, loss events, and reinsurance withdrawal—meaning the distribution is barbelled rather than uniformly positive.

A compact stakeholder-impact matrix:

| Stakeholder | Near-term effect | Medium-term effect | Geopolitical implication |

| Gulf exporters (oil/LNG) | Revenue upside if they can load and ship; severe downside if ports/terminals or transit are denied. | Investment and security costs surge; diversification to non-Hormuz routes becomes strategic priority. | Heightened reliance on external security guarantees; pressures regional alignment choices. |

| Europe gas buyers | Immediate price spike plus storage refill stress; competition with Asia intensifies. | Stronger policy push for demand management, electrification, and alternative LNG contracting structures. | Reinforces energy security as strategic policy pillar; sanctions and maritime security become linked. |

| Asian LNG buyers | Exposure to Qatar outage and Hormuz LNG concentration; higher spot competition. | Accelerated diversification to non-Qatar supply and regional storage where possible. | Potentially increases diplomatic pressure for de-escalation to protect economic stability. |

| Maritime insurers / P&I | Premium opportunity but extreme tail risk; formal cancellations indicate risk capacity withdrawal. | Market hardening and tighter clauses; sustained higher cost of capital for shipping. | Insurance becomes an enforcement lever shaping de facto navigation outcomes. |

| Governments with emergency stocks | Tool to dampen panic and buy time; decision speed matters. | Stock rebuild and strategic policy disputes over acceptable reserve levels. | Confirms energy resilience as national security; may reshape alliances and industrial policy. |

Indicators to watch for escalation, de-escalation, and likely stopping points

The most reliable de-escalation indicator is not rhetoric but underwriting. If war-risk cancellation notices are reversed, write-back coverage becomes widely available at tolerable cost, and major shipping lines resume transits through Hormuz with stable routing, that would signal a shift from “commercially closed” to “commercially open,” even if the war continues ashore. A second de-escalation marker is Qatar LNG restart confirmation and sustained cargo loading at Ras Laffan, because LNG is the marginal stressor in both Europe’s refill season and Asia’s prompt balancing. A third is the emergence of a credible diplomatic track with cessation of attacks on third-country territory and civilian infrastructure—an explicit demand in multiple official statements (UN, EU, China) that could function as a political “off-ramp” without resolving underlying nuclear and missile disputes.

Escalation indicators are more kinetic and more binary. Confirmed or suspected mining events, repeated successful strikes on tankers, or formal declarations that ships will be attacked if they attempt passage convert the risk from “priced” to “denied,” and tend to produce discontinuous price jumps. Expansion of strikes to critical export infrastructure across multiple Gulf states would imply a longer-duration outage profile and force a policy response (stock releases, demand restraint) that markets will price as evidence of structural scarcity. A final escalation marker is coalition normalization of “defensive action to destroy missiles at source,” which—while framed as proportional defense by some allies—creates an escalatory loop because it increases incentives for Iran to broaden its target set and for insurers to withdraw capacity.

As for stopping points, there are only a few that matter to markets. The first is restoration of an insurable maritime corridor through Hormuz (whether via negotiated non-attack commitments or naval enforcement). The second is the reconstitution of LNG deliverability (Qatar restart and/or durable alternative sourcing) in time for Europe’s injection season. The third is a political settlement that reduces the probability of renewed closure—because absent that, even a reopened strait may trade with a persistent risk premium embedded in prompt and seasonal contracts.