For most of their history, defence offsets have been treated by procurement officials and corporate counsel alike as a cost of doing business — a percentage figure buried in an annex, a schedule of industrial reinvestment obligations to be discharged over a decade, an administrative tail wagging behind the dog of the actual platform sale. That framing was never quite accurate, but in 2026 it has become actively misleading. The offset is no longer the tail. In a growing number of transactions, particularly those originating from or flowing into Türkiye, the industrial participation architecture is the substance of the deal, and the platform is merely the occasion for it. Understanding why this has happened, and what it means for the legal structuring of defence transactions, requires setting aside the inherited vocabulary and looking carefully at what buyers and sellers are now actually exchanging.

What an Offset Was — and Why the Old Model No Longer Holds

An offset, in its conventional form, obliges a foreign supplier to reinvest a defined proportion of contract value into the purchasing state’s economy. The mechanism splits into two families. Direct offsets attach to the contracted system itself — licensed local production, co-assembly of subcomponents, in-country final integration, transfer of manufacturing technology specific to the platform. Indirect offsets discharge the obligation through investment unrelated to the system sold, historically in civil aviation, education, or even sectors with no defence nexus whatsoever. For decades the indirect variety dominated, because it allowed primes to satisfy a nominal percentage requirement without surrendering the engineering know-how that constituted their actual competitive moat. A buyer received jobs and investment; the supplier retained its industrial secrets. Both sides could report success to their respective constituencies while the underlying capability gap remained exactly where it had always been.

That equilibrium has broken down, and it has broken down for reasons that are structural rather than cyclical. The first is the supply-chain shock that the war in Ukraine administered to every defence ministry that had outsourced its industrial base. When ammunition stockpiles emptied and resupply depended on production lines located in other sovereign jurisdictions, the strategic vulnerability of dependence became impossible to ignore. European states that had spent two decades treating domestic manufacturing as an inefficiency to be optimised away began mandating local or allied-territory production not as an offset sweetener but as a non-negotiable procurement condition. The second is the emergence of a class of buyer that is no longer purchasing capability at all, but rather purchasing an industrial base. Saudi Arabia, the largest defence spender in the Middle East and among the top global arms importers of the past five years, has made plain through its “look East” diversification that what it wants from suppliers is technology transfer, local manufacturing, and design localisation — the means of production, not merely its output. The third reason is the simplest: the Western monopoly on advanced systems has eroded. When fifth-generation aircraft, AI-enabled autonomous platforms, and precision-guided munitions came only from the United States and a handful of close allies, buyers had no leverage to demand technology transfer. The arrival of credible alternative suppliers willing to offer what the traditional primes withheld has rewritten the negotiating table, and the global market for offset and industrial participation services has grown accordingly, on a trajectory expected to roughly double over the coming decade.

Türkiye’s Domestic Offset Legal Framework: What Foreign Primes Must Understand First

Before examining how Turkish firms structure outbound offset packages for foreign customers, it is worth establishing the foundational instrument that governs the inbound side — the framework that any foreign prime or tier-one supplier encounters the moment it seeks to sell into the Turkish defence market. The Presidency of Defence Industries administers the Industrial Participation Programme, known in Turkish as the Sanayi Katılımı Programı, which obliges foreign suppliers in SSB-managed procurement to generate industrial participation credits equivalent to a defined percentage of the contract value, typically set at one hundred percent of the import component and in strategically significant programmes considerably higher. The programme distinguishes between direct industrial participation — contributions directly related to the contracted system, such as subcontracting to Turkish firms, licensed production, co-assembly, or technology transfer specific to the platform — and indirect industrial participation, covering investments in the broader Turkish defence and aerospace ecosystem including R&D collaboration, supplier development, and co-investment in Turkish industrial capacity. Credits are not fungible across all categories and are weighted differently depending on their strategic value to SSB’s industrial development objectives, a structuring dimension that experienced practitioners treat as the central variable in designing a cost-efficient industrial participation plan.

The mechanics of SSB’s credit-weighting and multiplier architecture deserve particular attention, because they determine a foreign prime’s commercial calculus more directly than any other feature of the programme. Contributions that transfer genuine engineering capability — co-development of subsystems, transfer of manufacturing process technology, establishment of R&D facilities in Türkiye, or creation of design authority within a Turkish entity — attract multipliers that can be materially higher than a one-to-one credit ratio, meaning that a strategically structured industrial participation plan can satisfy a nominally large obligation through a substantially smaller absolute investment than a straightforward component-procurement approach would require. Conversely, contributions that amount to routine subcontracting of standard items, or that involve Turkish entities as nominal intermediaries rather than genuine technical participants, will attract base-rate credits that make the arithmetic of obligation discharge considerably less favourable. The practical implication for a foreign supplier structuring its bid is that the industrial participation plan should be designed upstream — before pricing is finalised and before the commercial offer is submitted — because the credit efficiency of different participation categories directly affects the total cost of compliance, and that cost must be reflected in the offer price rather than discovered after contract signature. SSB’s evaluation of industrial participation plans is substantive rather than formal; a plan that is legally adequate but commercially thin will generate scrutiny, and the enforcement record of recent procurement cycles makes clear that SSB has both the institutional appetite and the procedural tools to hold foreign suppliers to the commitments they make at bid stage.

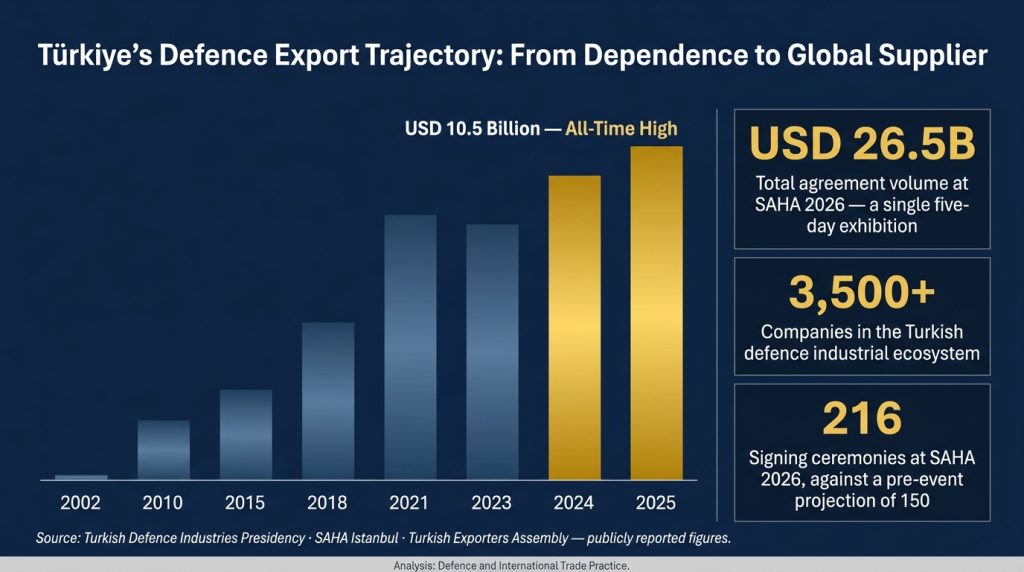

The administration of the programme is SSB’s exclusive domain, and the approval of an industrial participation plan — the formal document in which a foreign supplier commits its offset obligations, timelines, credit categories, and Turkish partners — is a condition of contract signature, not a post-award formality. This sequencing has practical consequences that foreign counsel frequently underestimate: the industrial participation plan must be credible, bankable, and legally structured before the commercial negotiation concludes, because SSB’s procurement process treats it as an integrated component of the bid rather than a supplementary undertaking. Default on industrial participation obligations carries financial penalties, and the enforcement culture has been materially more rigorous in recent procurement cycles than the more accommodating posture that characterised some earlier programmes. The broader policy context is also important: SSB’s industrial participation programme is not merely a procurement condition — it is the primary mechanism through which Türkiye’s defence industrial base has been built from near-total import dependence in the early 2000s to an export volume exceeding USD 10.5 billion in 2025, operating across more than 3,500 companies employing approximately 100,000 people. The SSB’s defence industrial development fund carries a 2026 resource estimate of approximately TRY 333 billion, and Türkiye’s stated export target for the current year exceeds USD 11 billion. For a foreign prime, navigating this framework competently is not a compliance exercise; it is the entry ticket to one of the most dynamic defence procurement markets in the alliance, and getting the industrial participation architecture wrong at the bid stage is a mistake that cannot be remedied after contract signature.

Türkiye as the Defining Case Study for the New Export Offset Model

It is against this domestic foundation that Türkiye’s outbound offset model becomes fully intelligible. The country has not simply developed competitive platforms; it has internalised, through decades of absorbing foreign industrial participation obligations, precisely what offset architecture looks like when it is designed to transfer genuine capability rather than discharge a nominal percentage. That institutional learning is now being deployed in Türkiye’s own export relationships with extraordinary effectiveness. The scale of the opportunity is visible in the numbers from a single month: SAHA 2026, held in Istanbul in May, produced a total agreement volume of USD 26.5 billion across 216 signing ceremonies, with Turkish firms as the primary

supply-side participants.

That figure is not merely a commercial milestone; it is the quantified expression of an export model in which the industrial participation architecture has become the primary source of competitive differentiation. Consider the structure of Baykar’s Kızılelma agreement with Indonesia, concluded at that exhibition. The transaction provides for an initial squadron of unmanned combat aircraft, but the substance of the agreement lies elsewhere: in the establishment of local production, maintenance, repair and overhaul facilities, integration centres, expert certification of Indonesian technical personnel, and a longer-term commitment to joint research into strategic technologies. The technology localisation is not an obligation attached to the sale of aircraft; it is the commercial offer itself. Indonesia is not buying drones. It is buying the capacity to make, sustain, and eventually evolve drones, and the aircraft delivered in the interim are a down payment on that capability. The depth of the resulting relationship is visible in the projection that a substantial majority of Indonesia’s UAV procurement spending over the next decade — estimated at approximately USD 2.3 billion — will flow to Turkish platforms, a market share built not on unit price but on Türkiye’s willingness to embed itself inside the customer’s sovereign defence ecosystem in a way no traditional supplier would countenance.

The same logic appears in a different register in the ARCA Baltics Operations facility signed at SAHA 2026, under which a Turkish manufacturer will construct a EUR 300 million ammunition plant at Estonia’s Põhja-Kiviõli Defence Industry Park, oriented primarily toward long-range 155mm artillery production for European and US markets. Here the offset structure has been inverted geographically. Türkiye is not exporting ammunition into NATO’s eastern flank; it is establishing itself as a manufacturer within NATO territory, positioning its output to qualify for European procurement frameworks and embedding its production capacity directly into the alliance’s resupply architecture. The Leonardo–Baykar joint venture, which contemplates a Turkish-designed loyal-wingman system assembled in Italy, pushes the same idea further still, raising the prospect of a platform that is Turkish in origin yet potentially European in regulatory classification — and therefore potentially eligible for the procurement budgets and defence-funding mechanisms reserved for EU-origin systems. These are not variations on a theme. They are distinct legal and industrial architectures, each engineered to achieve a strategic objective that a conventional export sale could never deliver. And the Saudi–Turkish technology transfer agreements of 2025, in which Saudi Arabian Military Industries formalised localisation arrangements with leading Turkish defence firms for advanced land systems manufacturing in the Kingdom, demonstrate that the same model reaches equally into the Gulf: the buyer is purchasing not hardware but the industrial capability to produce hardware domestically, and Türkiye has proven itself the most willing and capable vendor of that capability among the field of mid-tier suppliers.

The Offset as an Instrument of Foreign Policy

What unites all of these structures is that the modern offset has become, at its core, an instrument of foreign policy executed through corporate structuring. A state that manufactures Turkish-designed aircraft on its own soil, sustains them through Turkish-trained technicians, and runs Turkish autonomy and mission software within its command architecture has entered into an alignment with Türkiye that is far more durable than any diplomatic communiqué, precisely because it is industrial rather than rhetorical. The relationship is expensive to exit and painful to unwind, which is exactly the point. There is also a less discussed dimension worth naming directly: co-manufacturing creates mutual hostage value against third-party sanctions. When a buyer’s own production line depends on a technology source, sanctioning that source disrupts the buyer’s sovereign capability, which materially raises the political cost of any external attempt to interfere with the relationship. For buyers in regions exposed to extraterritorial enforcement risk, this insulating quality is not an incidental benefit; it is part of why localisation arrangements that earlier generations would have dismissed as needlessly complex are now actively sought.

Layered atop all of this is NATO’s own evolving posture, in which allied industrial capacity is increasingly treated as a collective security asset in its own right. In that frame, the Estonian ammunition facility simultaneously serves Turkish commercial interest, Estonian national security, and alliance-wide resupply resilience — a single offset structure discharging three different strategic functions at once. As Türkiye prepares to host the NATO Summit in Ankara in July 2026, and as the alliance moves to establish the most extensive defence industry forum in its history on the margins of that event, the embedding of Turkish manufacturing capacity within allied procurement architecture is not incidental to Türkiye’s alliance positioning. It is one of its most tangible expressions.

Where the Legal Weight Now Sits: Offset Obligation Versus Export-Control Permission

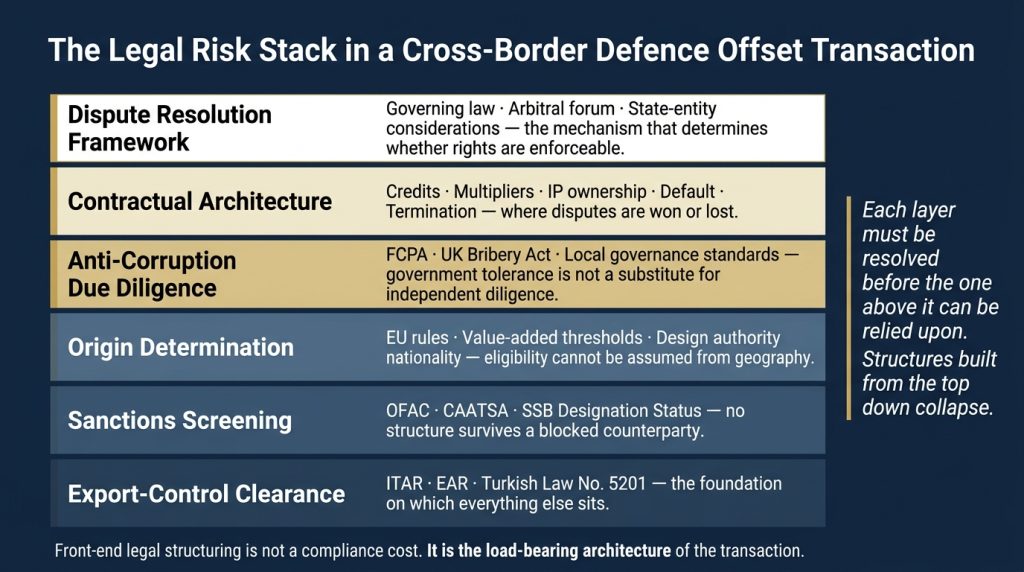

For the lawyer structuring these transactions, the elevation of the offset from administrative annex to strategic core has a direct and unforgiving consequence: the legal complexity has migrated to where the value now sits. The first and most persistent tension is between what an offset obligation requires and what an export-control regime permits. A procurement contract may oblige a supplier to transfer manufacturing technology, but the supplier’s freedom to do so is constrained by the export-control law of its home jurisdiction and, critically, by the law governing any third-country content embedded in the system. A Turkish prime offering co-production of an advanced fighter as part of an industrial participation package must reckon with the United States International Traffic in Arms Regulations to the extent the aircraft carries a US-origin engine or controlled subsystem, because the re-export and re-transfer of that content remains subject to US authorisation regardless of where the airframe is assembled or who assembles it. The obligation to transfer and the permission to transfer are governed by entirely different bodies of law, answerable to different sovereigns, and they are frequently in conflict. Resolving that conflict — through careful scoping of what technology actually crosses a border, through licensing strategy, through the architecture of what is built where — is not a compliance afterthought. It is the load-bearing element of the deal, and the burden of getting it right falls squarely on the supplier and its counsel.

Türkiye’s Own Export-Control and Dual-Use Architecture

A discussion of the legal framework governing offset and industrial participation structures involving Turkish entities would be incomplete without addressing Türkiye’s own domestic export-control regime, because it operates in parallel to — and sometimes in tension with — the international frameworks that receive greater attention in cross-border commentary. The foundational instrument is Law No. 5201 on the Control of Exports of Dual-Use Items and Technologies, supplemented by implementing regulations that align Türkiye’s control lists with the Wassenaar Arrangement, the Australia Group, the Missile Technology Control Regime, and the Nuclear Suppliers Group — the four principal multilateral export-control regimes to which Türkiye is a participating state. Licensing authority for controlled dual-use exports sits with the Ministry of Trade, while the export of military and defence items falls under the jurisdiction of SSB and the Ministry of National Defence, with the Undersecretariat of Defence Industries retaining an oversight role in transactions with industrial participation dimensions.

The instrument that has attracted the most sustained international attention in 2026 is Presidential Decision No. 11068, signed in March 2026, which established a structured authorisation regime for the transit and re-export of controlled military items through Turkish customs territory. The decree includes a catch-all provision extending its scope to items not expressly listed where there is a reasonable basis to suspect military end use or a risk to national or international security, and it vests the Ministry of Trade with authority to require an approval letter — an uygunluk yazısı — before covered shipments may proceed, as well as authority to revoke approvals already granted. The policy rationale is transparent: successive OFAC actions designating Turkish-linked entities for facilitating Iranian weapons procurement have created sustained pressure on Ankara to demonstrate that its customs territory cannot be used as a transshipment corridor for controlled technology, and Presidential Decision No. 11068 is the formal legislative response to that pressure. What it does not resolve — and what international commentators have noted directly — is the gap between the decree’s legal architecture, which is formally robust, and the enforcement record of the institutions charged with implementing it, which has been less consistent. For foreign suppliers and investors structuring transactions that involve Turkish intermediaries, logistics providers, or financial institutions, the practical consequence is that Turkish regulatory clearance does not foreclose scrutiny by OFAC, BIS, or equivalent authorities in third jurisdictions. The two analyses are independent, and the more stringent one governs.

Distributed Production, Re-Export Chains, and the Question of EU Origin

The complexity compounds further when production is distributed across jurisdictions, which is the defining feature of the new offset structures. When a component is manufactured at an offset facility in one country, incorporated into a system in a second, and ultimately delivered to an end-user in a third, the export-control chain becomes a sequence of distinct licensing events, each potentially governed by a different regime, each requiring its own end-user and end-use analysis. The Estonian ammunition facility is a clean illustration of the problem: artillery produced there for European and US markets will need to satisfy Estonian export licensing requirements, navigate the European Union’s dual-use and defence-related controls under Regulation 2021/821 and applicable Common Position instruments, and account for any US-origin content in propellant chemistry or production technology that might trigger US jurisdiction over downstream transfers — and these analyses must be completed before the first round leaves the line, not discovered during a compliance review triggered by a customer complaint or a regulatory inquiry.

Closely related is the question of EU origin, which in the current European context carries direct financial consequence of a magnitude that earlier offset structures did not encounter. As Turkish-designed systems are assembled within EU member states, whether the resulting product qualifies as EU-origin for procurement eligibility and for access to instruments such as the European Defence Fund, the Security Action for Europe regulation, and the European Defence Industry Programme is a determination that cannot be assumed from the geography of final assembly alone. It depends on value-added thresholds, on the provenance of critical components, on the classification of integrated software and data systems, and in some cases on the nationality of design authority. These rules of origin analyses require front-end legal opinions rendered before commercial commitments are priced on the assumption of eligibility. A misjudgement here does not merely create regulatory exposure; it can invalidate the entire commercial rationale for locating production in Europe in the first place, and it can expose a party to procurement-fraud liability if eligibility was represented to a procuring authority on an insupportable basis.

Anti-Corruption Exposure in Offset Administration

There is a further dimension that experienced practitioners ignore at their peril, because it has historically generated more enforcement liability than any technical export-control violation: the anti-corruption exposure inherent in offset administration. Offset programmes have long ranked among the highest-risk environments for improper intermediary arrangements, precisely because they involve large discretionary value transfers, government counterparties, and the use of local agents and partners in jurisdictions with varying governance standards. The mechanism is familiar: an offset obligation creates an incentive for the foreign supplier to channel investment through intermediaries who can credit-generate quickly; those intermediaries frequently have political connections that explain their effectiveness; and the line between legitimate facilitation and improper inducement is one that enforcement authorities on both sides of the Atlantic have shown themselves very willing to scrutinise in retrospect. The point is not abstract. Where a counterparty’s ownership has attracted public governance scrutiny — as has been the case with certain prominent participants in recent high-profile offset signings — the fact that a buyer government has elected to proceed regardless does not discharge the diligence obligations of the supplier, the financier, or any third party relying on that transaction. A government’s tolerance of a counterparty is not a substitute for independent due diligence under the Foreign Corrupt Practices Act, the UK Bribery Act, or their analogues, and a contractor who treats the former as covering the latter has profoundly misunderstood where the liability ultimately lands.

The Contractual Architecture of the Offset Agreement

The strategic and regulatory dimensions of a modern offset transaction are ultimately realised — or frustrated — at the level of the contract, and it is there that disputes originate and that counsel provides its most immediate and defensible value. The definition and verification of offset credits is frequently the most contested element: credits must be defined with sufficient precision to be measurable, the verification mechanism must be agreed before obligations arise rather than negotiated under the pressure of a default allegation, and the treatment of disputed credits — who bears the burden of proof, what documentation is required, what the cure period looks like — must be explicit rather than left to implication. Multiplier mechanisms, which award enhanced credit for high-value or technology-intensive contributions, create their own interpretive disputes when the categorisation of a contribution is ambiguous, and the drafting of multiplier thresholds requires the same specificity as any other defined term in a long-term commercial agreement.

The consequences of offset default and the enforceability of penalty clauses raise questions that vary materially across jurisdictions: a penalty clause structured as liquidated damages may be enforceable under one governing law and characterised as an unenforceable penalty under another, and where the offset counterparty is a state entity — as it frequently is in Turkish procurement — the intersection of private contract law, administrative law, and sovereign immunity doctrine creates a layer of analysis that must be addressed before a dispute arises rather than after. Intellectual property ownership in co-production arrangements is among the most negotiated and most litigated issues in offset practice: who owns improvements to a licensed design, what happens to locally developed derivative works, and how manufacturing know-how transferred under an offset is protected against replication in successor programmes that do not carry equivalent obligations are questions whose answers must be explicit in the agreement, because no implied term will resolve them satisfactorily in the context of a relationship that may span fifteen years and multiple technology generations. Finally, the interaction between offset obligations and sanctions-triggered termination events has moved from a theoretical drafting concern to an operationally urgent one: a transaction structured today may encounter a sanctions designation, an OFAC action affecting a counterparty, or a change in US policy toward a third-country technology source at any point during a ten-year offset period, and the agreement must have a clear and legally tested mechanism for addressing those events without leaving either party in an impossible position.

Governing Law and Dispute Resolution: The Turkish State-Entity Question

The choice of governing law and dispute resolution forum is never more consequential than in an offset agreement where one party is a Turkish state entity, and it is a question that requires resolution at the drafting stage rather than at the point of dispute. Turkish state entities, including SSB, operate under a legal framework that combines elements of public administrative law with commercial contracting practice, and the interaction between these bodies of law produces outcomes that differ materially from what a foreign counterparty accustomed to purely commercial arbitration might expect. Turkish administrative courts retain jurisdiction over disputes arising from public procurement contracts in certain circumstances, and the boundary between an administrative act and a commercial contractual dispute — relevant where SSB exercises its regulatory authority in a manner that affects a foreign supplier’s offset obligations — is not always drawn with the clarity that international practitioners prefer.

International arbitration clauses in contracts with Turkish state entities have historically been subject to resistance at the drafting stage and, in some cases, to jurisdictional challenge after disputes arise. The Istanbul Arbitration Centre provides a domestic institutional framework with increasing familiarity among Turkish state procurement counterparties, and it offers procedural rules that are compatible with international standards while being situated within Turkish legal geography in a way that can reduce some of the political friction associated with fully international forums. For transactions of the scale and duration typical of major offset programmes, the ICC International Court of Arbitration and ICSID remain the preferred forums for many foreign counterparties, but their availability depends on the specific contractual language agreed and, in some cases, on the existence of applicable bilateral investment treaties. The enforceability of interim relief in Turkish courts — a critical practical question in disputes where a party seeks to preserve the status quo pending the outcome of arbitral proceedings — is an area that has evolved in recent years but that still requires case-specific analysis rather than reliance on general principle. The overarching point is that the governing law and dispute resolution architecture of an offset agreement involving Turkish state entities must be negotiated with the same rigour and the same front-end investment of legal analysis as the credit definitions and multiplier thresholds — because in a programme of fifteen-year duration, the probability that it will matter is not theoretical.

A Working Typology of 2026 Offset Structures

It is useful, against this legal backdrop, to organise the contemporary landscape into a working typology, because the regulatory analysis differs materially across structures and conflating them produces error.

The first structure is the embedded production offset, in which a foreign supplier builds a manufacturing facility within the buyer’s territory; the buyer acquires sovereign production capacity and the supplier acquires market access and a durable supply-chain relationship, with the principal legal questions concentrated in host-state licensing, technology-transfer authorisation, and origin determination. The second is the technology-ecosystem offset, in which a platform sale is wrapped in MRO infrastructure, training, software integration, and long-term research cooperation; here the controlled item is frequently intangible — technical data, source code, training curricula, sustainment know-how — and the export-control analysis must extend well beyond hardware to the deemed-export and technical-assistance rules that govern the transfer of knowledge itself. The third is the joint-venture co-production offset, in which firms from different states establish a shared manufacturing entity whose output may qualify for procurement in multiple jurisdictions; the defining legal challenge is jurisdictional layering, since two or more export-control regimes, two or more origin frameworks, and two or more sets of procurement-eligibility rules apply simultaneously to a single production stream. The fourth is the technology-transfer localisation offset, in which the supplier conveys design, process, and engineering know-how to a manufacturer in the buyer state; this structure carries the deepest transfer of value and correspondingly the most acute control sensitivity, because it implicates not only what is built but the capacity to design successor systems, and it sits closest to the proliferation concerns that the controlling regimes were written to address.

The Unresolved Tensions: Proliferation, Dependency, and Compliance Arbitrage

Those proliferation concerns deserve candid acknowledgement rather than diplomatic elision, because they constitute the genuine unresolved tension at the centre of the new offset economy. Technology-transfer offsets for autonomous systems, long-range precision weapons, and AI-enabled platforms open pathways that the architecture of arms embargoes and traditional export controls was simply not designed to police. An offset factory situated in a third country is structurally far more difficult to sanction than a direct export shipment, and the diffusion of advanced military technology through industrial participation rather than finished-goods transfer is a phenomenon that the controlling regimes are only beginning to confront. There is, too, the paradox at the heart of the buyer’s bargain: the sovereign capability acquired through a localisation offset is frequently far less sovereign than it appears, remaining dependent on the original supplier for software updates, propulsion components, guidance modules, and the sustainment expertise without which assembled platforms degrade into static displays. Genuine industrial autonomy requires the underlying design and engineering base, and that is precisely the element most localisation agreements are carefully drafted to withhold. Finally, and most uncomfortably for practitioners in tightly regulated jurisdictions, there is the dynamic of compliance arbitrage. Suppliers operating under more permissive control regimes, or under regimes enforced with less rigour, can offer technology-transfer terms that suppliers bound by ITAR, the Export Administration Regulations, and comparable frameworks simply cannot lawfully match. Buyers, rationally, gravitate toward the more generous offer, with the perverse result that the discipline of a supplier’s compliance regime can become a commercial handicap. This is not a hypothetical concern; it is a structural feature of a market in which the willingness to transfer has become the currency of competition.

The Regulatory Horizon: Frameworks in Motion

The analysis above reflects the regulatory environment as it stands in mid-2026, but practitioners making long-term structural commitments need to understand that this environment is itself in material motion, and that offset structures designed on today’s regulatory assumptions must be built with the capacity for amendment and adaptation. At the European level, the SAFE regulation and the European Defence Industry Programme are actively reshaping what qualifies as European for procurement and funding purposes, and the detailed implementing rules — particularly on origin and on the treatment of third-country components in jointly produced systems — are still being finalised. A structure that qualifies for EU funding eligibility today may not qualify under the tightened criteria expected to apply in the programme’s subsequent phases, and offset agreements with European industrial participation dimensions should contain explicit representations and review mechanisms tied to regulatory change rather than assuming static eligibility. In the United States, the administration is actively reviewing how ITAR applies to technology transferred through co-production arrangements with non-traditional allies, and the treatment of deemed exports — the transfer of controlled technical data to foreign nationals working within a co-production facility — is an area of ongoing enforcement attention that will affect every offset structure involving US-origin content in a multinational manufacturing environment.

For Türkiye specifically, the two most significant near-term regulatory variables are the enforcement trajectory of Presidential Decision No. 11068 and the resolution, or continued irresolution, of the CAATSA Section 231 designation of SSB. If the CAATSA designation is formally lifted — which requires written authorisation, statutory certification by the Secretaries of Defense and State, and Congressional notification, none of which has yet occurred notwithstanding the constructive political signals that have accompanied ongoing diplomatic engagement — the range of offset structures available to Turkish entities engaging with US-origin technology will expand materially. Until that formal instrument is issued, SSB’s designation status continues to constrain the industrial participation architectures available to any party whose transaction touches the SSB ecosystem, regardless of the political signals that have accompanied the ongoing diplomatic process. Practitioners who structure transactions today on the assumption that CAATSA relief is imminent are making a legal error with potentially serious commercial consequences, and the appropriate posture remains to design for the regulatory environment that exists rather than the one that is anticipated.

Conclusion: The Offset Is the Deal

The defence offset has ceased to be a percentage in an annex and has become the primary mechanism through which states now build durable strategic alignment, and Türkiye, by deliberate design, sits at the centre of that transformation as both an originator of outbound industrial-participation structures and an increasingly significant destination for inbound ones. For any party structuring these transactions — the foreign prime weighing a Turkish offset obligation under SSB’s industrial participation programme, the Turkish exporter designing a localisation package for a Gulf or Indo-Pacific customer, the financier underwriting a cross-border production facility, the European partner assessing origin and eligibility under evolving EU frameworks — the operative reality is that the legal weight of the transaction has moved to the same place the strategic value has moved: into the industrial-participation architecture itself. The deals being signed in 2026 carry export-control, sanctions, origin, anti-corruption, contractual, and dispute-resolution consequences of an order entirely different from the equivalent transactions of five years ago, and they demand to be structured from the front end by counsel who understand not only the strategic logic of what is being built but the full legal architecture required to make it durable, defensible, and capable of surviving the regulatory turbulence that the next decade will inevitably deliver. The transactions that succeed will be those whose industrial ambition and legal architecture were designed together, as a single integrated instrument, by people who treat the regulatory framework not as a constraint to be managed after the fact but as the very material from which a lasting transaction is built. In defence offset practice, there is no longer any meaningful distinction between the strategic adviser and the legal one. The offset is the deal, and the deal is the law.